- Investment strategy – maintain and build allocations: The Middle East war raises questions about the resilience of Asia’s economy to an energy shock. In our view the structural investment case for Developed Asia’s real estate is unchanged in a diversified portfolio with the advantage of a more favourable urban demographic outlook compared to the U.S. and Europe. Headwinds from higher energy costs warrant monitoring, but this energy disruption is a pricing event; not a structural economic reversal. Investors should seek to deploy capital judiciously and treat the current uncertainty as an entry window.

- Oil prices (c.$100/bbl. today): Current prices require no defensive action on existing allocations, as they are well short of the $130/bbl. reached at the onset of the Russia–Ukraine war, and far below levels that could cause structural economic damage.

- Critical threshold (oil price of $130/bbl. sustained for 60+ days): Duration matters more than the price level alone. A brief spike to $130/bbl. is manageable; the same price sustained for three months or more risks a marked global slowdown and a potential rise in unemployment. The latter is also likely to trigger interest rate cuts though the timing is highly uncertain. The potential for rate cuts is reinforced by a new Fed governor who is expected to favour easier policy in the United States.

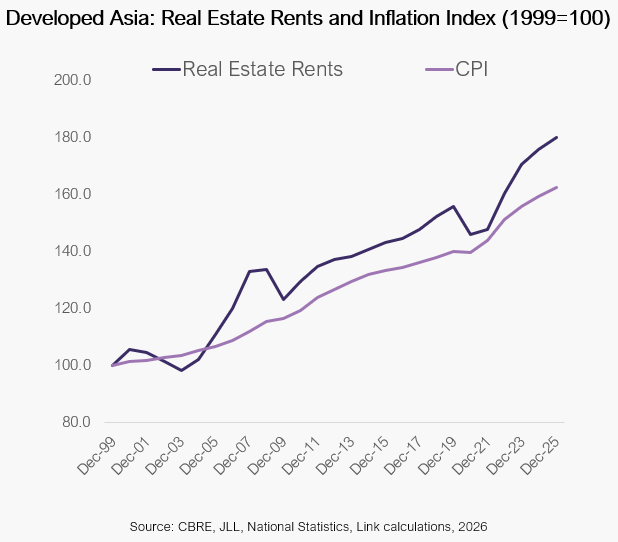

- Negative real rates and limited development support real asset values: With nominal rates near 2% across Developed Asia and inflation running at 2% on average, central banks have meaningful room to act should economies slow down significantly. Rate cuts will most likely result in negative real interest rates, directly supporting real asset valuations, as will limited new property supply. Higher inflation in Asia typically feeds through to higher rents which is also supportive to the market.

- Country differentiation: Japan, South Korea and Singapore face the greatest near-term risk from energy supply disruption; Hong Kong and Singapore carry risk through financial market channels; China is insulated by strategic reserves and substitution to coal; Australia benefits as a net energy exporter. Among major Asian economies, India is the most exposed. Even in a severe scenario, disruption for much of Asia is transitional as new supply chains establish within six months.

To request the full report, please reach out to us at LP@laml.com.