- Policy tightening resumes. The RBA raised the cash rate 25bps to 3.85% in response to underlying inflation running above the 2–3% target band in 2H 2025, with unemployment still low at 4.1%.

- Limited scope for further hikes. Recent inflation strength is partly driven by temporary factors that should fade. Labour market indicators are normalising, supporting the view that further significant rate tightening in 2026 is unlikely.

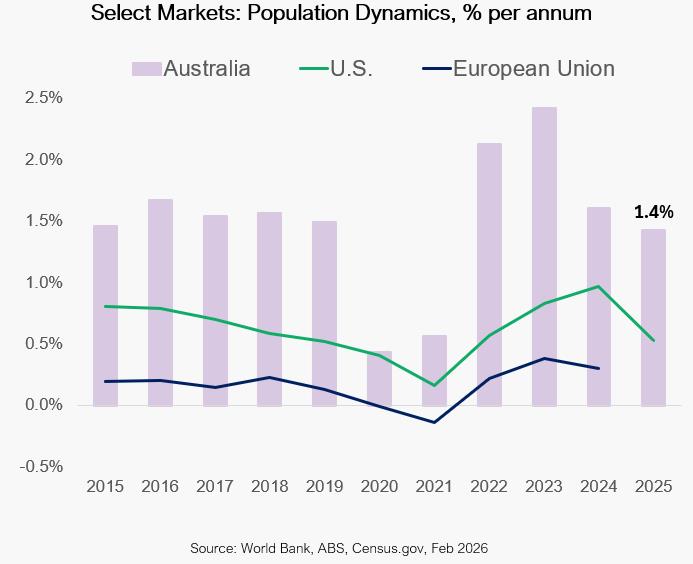

- Real estate fundamentals remain supportive. Robust population growth that is well ahead of the U.S. and the E.U., is sustaining occupier demand and rental growth. With development completions forecasted to be ~40% below the 2020 peak in 2026–27, the rental outlook remains positive.

- Short-term jitters which may create attractive opportunities. Higher rates are a near-term headwind for investors, but we don’t expect any significant impact on valuations as real estate fundamentals are strengthening; investor uncertainty could create attractive opportunities as local funds seek to raise liquidity amid redemption requests.

To request the full report, please reach out to us at LP@laml.com.