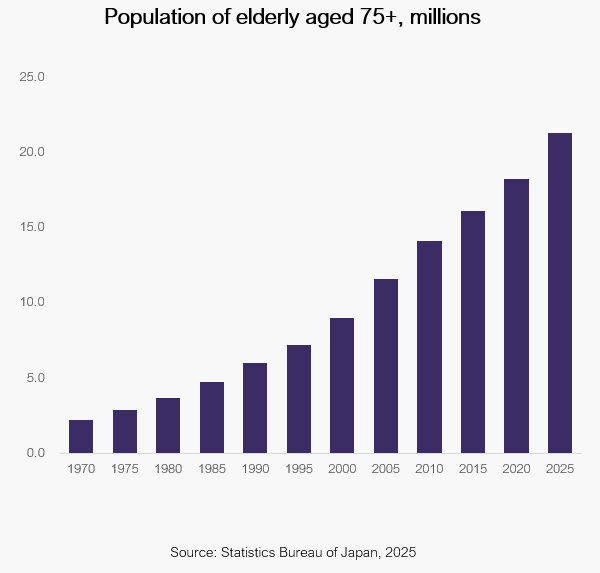

- Japan’s aged care real estate sector is supported by strong demographic fundamentals – in particular, the 75+ year old population is expected to have grown by 17% in the last 5 years, driving a sharp rise in high-acuity care needs.

- At the same time, the share of elderly living alone or as couples without nearby family continues to grow, limiting their access to support as they age. These structural trends are expected to drive strong ‘non-discretionary’ demand for aged care facilities.

- The supply of aged care facilities is constrained by tight government regulations, and by competition with other commercial uses such as multifamily real estate. The result is a persistent demand-supply imbalance, evident from the fact that annual beds additions represent only 10% of the annual rise in the 75+ year old population over the past five years.

- Affordability for aged care facilities is supported by a robust government backstop, funded equally through taxation and mandatory care insurance. The substantial financial and real estate wealth of Japan’s middle-class population also underpins aged care demand.

- Consistent public policy support has enabled the emergence of high quality and well-capitalised aged care operators. Major institutions have the confidence to allocate capital to the sector, enjoying high quality long-duration lease income.

- Japan’s aged care real estate offers the potential for durable cashflows at yields of 50 to 100bps above multifamily real estate, with stable occupancy rates of c. 90-95%.

- Investors can find opportunities across the risk spectrum: value-add strategies include build-to-suit developments or the repositioning and redevelopment of older assets to deliver strong risk-adjusted returns. Core strategies include sale-and-leaseback arrangements with owner-operators to provide stable and long-term income.

To request the full report, please reach out to us at LP@laml.com.