- Japan stands out as one of the few major office markets globally where occupier demand has strengthened through the post-pandemic period. Tokyo’s overall vacancy rate has fallen to 1.6% today, among the tightest of any major CBD office market globally.

- The strength of occupier demand reflects structural features of the Japanese economy: rising corporate profitability driven by a decade of governance reform, growing private capital markets fostering business formation, and persistently low remote work adoption relative to the U.S. and Europe. Taken together, these factors support ongoing employment growth in office-using sectors with limited near-term risk from AI-driven labour displacement.

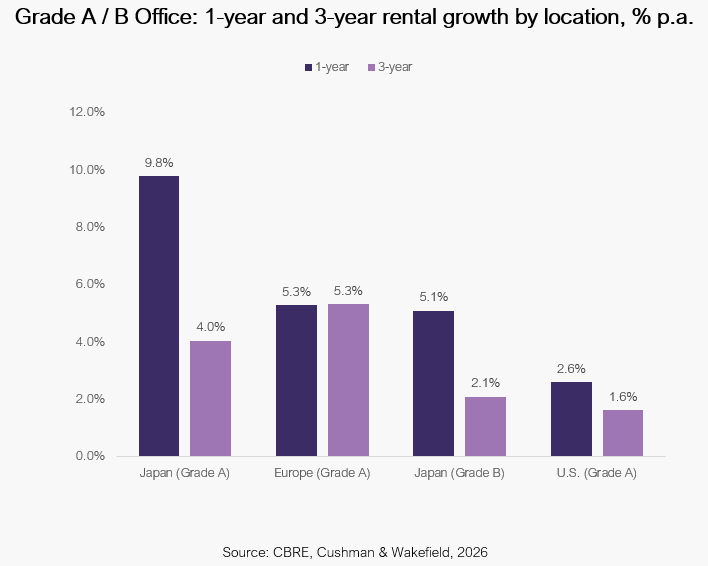

- In Japan, its large SME base, which employs approximately 75% of the workforce, drives a breadth of office demand that extends well beyond Grade A offices. In our view, Grade B offices offer the most compelling investment opportunity today: strong occupier demand aligned with SME requirements, higher transaction liquidity relative to tightly held Grade A stock, and a more favourable supply outlook as development economics constrain new mid-sized completions.

- Rents remain approximately 26% below their 2007 peak, a gap that signals significant further rental recovery ahead while we also see limited supply risk.

- Against a backdrop of gradual BoJ rate normalisation, our analysis shows Japanese office yields have historically tracked occupier conditions more closely than bond yields, and current fundamentals are robust.

- Our preferred strategy is to acquire under-rented, under-managed Grade B assets in Tokyo and Osaka for active repositioning: a value-add approach that drives rental uplift while providing downside protection in a rising rate environment.

To request the full report, please reach out to us at LP@laml.com.